The stablecoin bill GENIUS Act has been passed. Which cryptoassets will benefit from it?

2025-05-26 10:53

2025-05-26 10:53The sentiment in the cryptocurrency market is once again focused on regulatory actions.

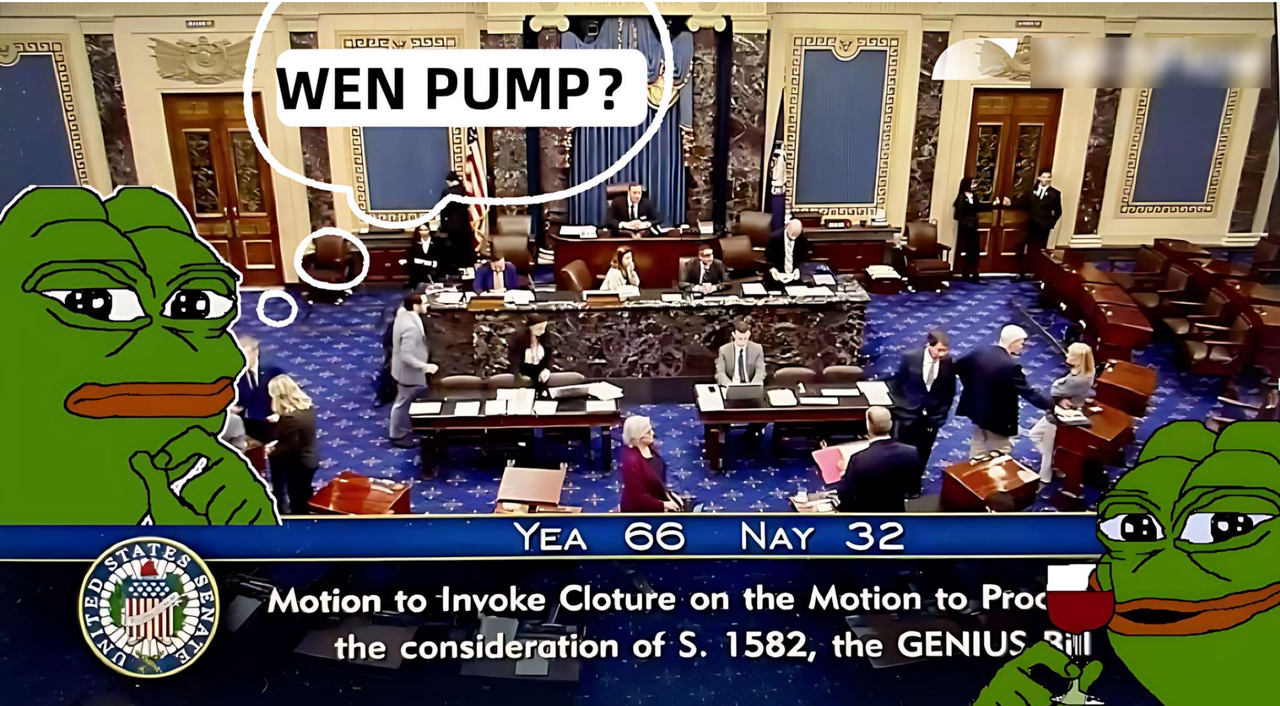

On May 19th, the US Senate passed the GENIUS Act ("2025 US Stablecoin Innovation Guidance and Establishment Act") by a vote of 66-32, marking a milestone in the upcoming implementation of the US stablecoin regulatory framework. As the first comprehensive US federal stablecoin regulatory act, the advancement of the GENIUS Act has quickly sparked a warm response in the cryptocurrency market, with the DeFi and RWA sectors related to stablecoins leading the market today.

Will the GENIUS Act become a catalyst for a new bull market?

According to Citibank's prediction, the global stablecoin market is expected to reach $1.6 to $3.70 trillion by 2030. The passage of the bill provides more qualitative and development space for stablecoins' "compliance", and traditional companies have more reasonable reasons to enter. The market is also looking forward to the influx of incremental funds, which can bring about a "flood of liquidity" and inject new liquidity into related cryptoassets.

But before that, you should at least understand what this bill actually contains and the legislative motivation behind it, in order to provide more convincing reasons for selecting relevant cryptoassets.

From "wild growth" to standardization

GENIUS Act, literally translated as "Genius Act", is actually an abbreviation of the "Guiding and Establishing National Innovation for U.S. Stablecoins Act of 2025". Simply put, it is a legislative document of the US government.

The reason why the market is paying attention is that it is the first comprehensive federal regulatory bill for stablecoins in US history. Prior to this, stablecoins and cryptocurrencies have always been in a subtle gray area: there is no explicit prohibition by law, but there are no clear rules telling you "how to do it". The goal of the GENIUS Act is to provide legitimacy and security for the stablecoin market through a clear regulatory framework, while consolidating the dominant position of the US dollar in digital finance .

In summary, the key contents of the bill include:

- Reserve requirements: The stablecoin publisher must have 100% reserve support, and the reserve assets must be highly liquid assets such as US dollars and short-term US Treasury bonds, and the reserve composition must be publicly disclosed every month.

- Regulatory classification: Large publishers (such as Tether and Circle) with a market value of more than $10 billion are subject to direct regulation by the Federal Reserve System or the Office of the Comptroller of the Currency (OCC), while small publishers can be regulated by states.

- Transparency and compliance: Prohibit misleading marketing (such as claiming that stablecoins are guaranteed by the US government), and require publishers to comply with Anti Money Laundering (AML) and Know Your Customer (KYC) regulations. Publishers with a market capitalization of more than $50 billion need to audit their financial statements annually to ensure transparency.

This means that the US's attitude towards stablecoins is actually friendly, but the premise is that stablecoins must be held in US dollars and meet the requirements of openness and transparency.

Looking back at history, the birth of the GENIUS Act was not achieved overnight, but rather the culmination of years of stablecoin regulation exploration in the US. We have also quickly sorted out the full timeline of this act to help you quickly understand its background and motivation.

The stablecoin market is developing rapidly, but the risks caused by regulatory deficiencies are becoming increasingly prominent. For example, the collapse of the algorithmic stablecoin UST in 2022 highlighted the need for clear regulation.

As early as 2023, the House Financial Services Committee proposed the STABLE Act, attempting to establish a regulatory framework for stablecoins, but it failed to pass the Senate due to bipartisan differences. On February 4, 2025, Senator Bill Hagerty, along with bipartisan lawmakers Kirsten Gillibrand and Cynthia Lummis, officially proposed the GENIUS Act, aiming to balance innovation and regulation. On March 13, the bill passed the Senate Banking Committee with a vote of 18-6, demonstrating strong bipartisan support. However, the first unanimous vote on May 8th failed because it did not reach the 60-vote threshold (48-49), and some Democratic lawmakers (such as Elizabeth Warren) were concerned that the bill could benefit Trump family crypto projects (such as USD1 stablecoin), believing that there was a conflict of interest.

After revision, the bill added restrictions on big tech companies, eliminated concerns about conflicts of interest among some lawmakers, and finally passed a procedural vote on May 19 with a vote of 66-32, and is expected to pass the Senate with a simple majority vote soon.

So, what is the significance of legislation reaching this point?

First, the market wants certainty. The passage of the bill essentially marks the US stablecoin market moving from "wild growth" to standardization, filling a long-standing regulatory gap and providing certainty to the market.

Secondly, it is obvious that it wants to consolidate the position of the US dollar through stablecoins, especially under the competitive pressure of China's digital yuan and the European Union's MiCA regulations.

Finally, the advance of the GENIUS Act could pave the way for broader crypto market legislation, such as the Market Structure Act, to promote the integration of the crypto industry with traditional finance, providing a legal basis for breaking into other demographics.

Cryptoassets related to interests

The core provisions of the GENIUS Act directly affect the stablecoin ecosystem and spread to the entire cryptocurrency market through a chain reaction. This regulatory framework will not only reshape the stablecoin industry, but also affect multiple cryptocurrency tracks such as DeFi, Layer 1 blockchain, and RWA through the widespread application of stablecoins. However, some projects in these tracks do not fully meet the regulatory requirements of the Act. If the Act is to be seen as a positive development, corresponding adjustments need to be made in product design and business.

We have sorted out some relatively large projects and listed the benefits and adjustments as follows.

- Centralized stablecoin publisher:

The reserve requirements of the bill (100% Current Asset, holding US Treasury bonds) and transparency regulations (such as monthly disclosure) are most favorable for centralized stablecoins. These stablecoins have basically met the requirements, and regulatory clarity will attract more institutional funds to enter and expand their use in trading and payment fields.

$USDT (Tether): USDT is the largest stablecoin by market value (about $130 billion in 2025), with about 60% of its reserves being US short-term government bonds (about $78 billion) and 40% being cash and cash equivalents (data source: Tether 2025 Quarter 1 Transparency Report). The GENIUS Act requires reserve assets to be mainly US bonds, and Tether fully complies with this requirement, and its transparency measures (such as quarterly audits) also meet the requirements of the Act. However, the key point is that the use of USDT has always had a gray industry part (such as fraud), and how to adjust the business to adapt to regulation is the next issue to be considered.

$USDC (Circle): The market value of USDC is about 60 billion US dollars, with 80% of its reserves being short-term US Treasury bonds (about 48 billion US dollars) and 20% being cash (data source: Circle's May 2025 monthly report). Circle has been registered in the US and actively cooperates with regulations (such as applying for an IPO in 2024), and its reserves fully comply with the requirements of the bill. The passage of the bill may make USDC the preferred stablecoin for institutions, especially in the DeFi field (USDC's share in DeFi has reached 30% by 2025), and its market share is expected to further increase.

- Decentralized stablecoins :

$MKR (MakerDAO, publish DAI): DAI is the largest decentralized stablecoin (market value about $9 billion), published through over-collateralized crypto assets (such as ETH), about 10% of the current reserves are US Treasury bonds (about $900 million), mainly collateralized by crypto assets (data source: MakerDAO May 2025 report). The strict requirements of GENIUS Act on reserve assets may pose a challenge to DAI, but if MakerDAO increases the proportion of US Treasury reserves, it can benefit from the overall market growth. $MKR holders may profit from the increase in DAI usage (the annual income of MakerDAO protocol in 2025 is about $200 million).

$FXS (Frax Finance, publish FRAX): The market value of FRAX is about 2 billion US dollars, using some algorithmic mechanisms (50% collateral, 50% algorithm), and about 15% of the collateralized assets are US bonds (about 300 million US dollars). If Frax adjusts to a full collateral model and increases the proportion of US bonds, it can benefit from market expansion, but its algorithmic mechanism may face regulatory pressure because the bill does not protect algorithmic stablecoins.

$ENA (Ethena Labs, publish USDe): USDe has a market value of about $1.40 billion, published through ETH hedging and yield strategy, and only 5% of its reserves are US bonds (about $70 million). Its strategy may need to be significantly adjusted to comply with the requirements of the law. If successful, it can benefit from market growth, but there are also risks involved.

- DeFi Trading/Lending

$CRV (Curve Finance): Curve focuses on stablecoin trading (TVL about $2 billion in 2025), with 70% of its liquidity pool being stablecoin trading pairs (such as USDT/USDC). The increase in stablecoin usage driven by GENIUS Act will directly increase Curve's trading volume (current daily trading volume is about $300 million), and $CRV holders can benefit from transaction fees (annualized return of about 5%) and governance rights. If the stablecoin market follows Citi's forecast, Curve's TVL may increase by another 20%.

$UNI (Uniswap): Uniswap is a universal DEX (TVL is about 5 billion USD in 2025), and stablecoin trading pairs (such as USDC/ETH) account for 30% of its liquidity. The increase in the active level of stablecoin trading brought by the bill will indirectly benefit Uniswap, but its benefits are lower than Curve (due to more diversified business). $UNI holders can benefit through transaction fees (about 3% annualized).

$AAVE (Aave): Aave is the largest lending protocol (TVL about $10 billion in 2025), and stablecoins (such as USDC, DAI) account for about 40% of its lending pool. The passage of the bill will attract more users to use stablecoins for lending (such as mortgaging USDC to borrow ETH), and Aave's deposits and borrowings may further increase (based on current trends). $AAVE holders benefit from protocol revenue (annual revenue about $150 million in 2025) and token value increase.

$COMP (Compound): Compound's TVL is about $3 billion, and stablecoin lending accounts for about 35%. Similar to Aave, the increase in stablecoin lending will benefit Compound, but its market share and innovation speed are lower than Aave, so the potential increase of $COMP may be relatively small.

- Revenue agreement

$PENDLE (Pendle): Pendle focuses on income tokenization (TVL about $500 million in 2025), and stablecoins are often used in its income strategy (such as the USDC income pool, with a current annualized return of about 3%). The growth of the stablecoin market driven by the bill will increase Pendle's income opportunities (such as the return rate may rise to 5%), and $PENDLE holders may benefit from the growth of protocol income (annual income about $30 million in 2025).

- Layer1

$ETH (Ethereum): Ethereum hosts 90% of stablecoin and DeFi activity (DeFi TVL will exceed $100 billion by 2025). The increase in stablecoin usage driven by the bill will increase the transaction volume on the Ethereum chain (current Gas fee annual income is about $2 billion), and the value of $ETH may rise due to demand growth.

$TRX (Tron): Tron is an important network for the circulation of stablecoins. Public data shows that in 2025, the circulation of USDT on the Tron chain will be about 60 billion US dollars, accounting for 46% of the total USDT; the increase in the use of stablecoins promoted by the bill may enhance the on-chain activities of Tron.

$SOL (Solana): Solana has become an important platform for stablecoins and DeFi due to its high throughput and low cost (TVL is about $8 billion in 2025, and on-chain USDC circulation is about $5 billion). The increase in stablecoin usage will drive Solana's DeFi activity (current daily trading volume is about $1 billion), and $SOL may benefit from the increase in on-chain active level.

$SUI (Sui): Sui is an emerging Layer 1 (TVL about 1 billion USD in 2025) that supports stablecoin-related applications (such as Thala's stablecoin and DEX). The growth of the stablecoin ecosystem driven by the bill will attract more projects to deploy on Sui, and $SUI may benefit from the improvement of the ecosystem's active level (current daily active users are about 500,000).

$APT (Aptos): Aptos is also an emerging Layer 1 (TVL about 800 million USD in 2025), and its ecosystem supports stablecoin payments. The increase in stablecoin circulation will drive Aptos' payments and DeFi applications, and $APT may benefit from user growth.

- Payment racetrack

$XRP (Ripple): XRP focuses on cross-border transfer (with an average daily transaction volume of about 2 billion USD in 2025), and its low cost and high efficiency characteristics can complement stablecoins. The increased demand for stablecoins for cross-border transfer driven by the bill (such as USDC for international settlement) will indirectly enhance the usage scenarios of XRP (such as as as a bridge currency), and $XRP may benefit from the growth in payment demand.

$XLM (Stellar): Stellar is also focused on cross-border transfer (average daily transaction volume of about $500 million in 2025), and has collaborated with IBM to launch the World Wire project, using stablecoins as bridge assets.

- Oracle

$$LINK +$$PYTH: The oracle provides price data for stablecoins and DeFi. The expansion of the stablecoin market driven by the bill will increase the demand for real-time price data in DeFi, and the amount of on-chain data calls may increase. However, this is more like an extension of the sector's bullish logic, rather than a complete strong correlation.

- RWA

$ONDO (Ondo Finance): Focusing on tokenizing Fixed Income assets such as US Treasury bonds, its flagship product USDY (a stable income token supported by US Treasury bonds) has been published on chains such as Solana and Ethereum (the circulation of USDY in 2025 is about 500 million US dollars). The GENIUS Act requires stablecoin reserves to hold US Treasury bonds, which directly benefits Ondo's US Treasury tokenization business. USDY may become one of the preferred reserve assets for stablecoin publishers. In addition, the increase in stablecoin circulation will drive retail investors and institutions to purchase USDY through USDC, and Ondo's asset tokenization demand may increase, benefiting $ONDO holders.

The dollar, a bigger conspiracy

The US is promoting stablecoin legislation, which can be considered a "strategy". On the one hand, the US hopes to weaken the US dollar policy and increase exports, but on the other hand, it does not want to give up the status of the US dollar as a global currency. By supporting the development of stablecoins, the US has extended the global influence of the US dollar in a digital way without increasing the debt of the Federal Reserve - currently 99% of stablecoins are pegged to the US dollar.

At the same time, the regulatory requirement that stablecoins must hold US short-term Treasury bonds as reserves cleverly found new buyers for US bonds, just as Tether's holdings of US bonds have surpassed many developed countries. This policy not only maintains the global dominance of the US dollar, but also finds reliable buyers for the huge US debt, killing two birds with one stone. The passage of the GENIUS Act is undoubtedly a milestone in the cryptocurrency market. By binding stablecoins and US bonds, it provides a new path for the continuation of US dollar hegemony and promotes the comprehensive prosperity of the cryptocurrency ecosystem.

However, this "open strategy" is also a double-edged sword - while bringing opportunities, its high dependence on US bonds, potential suppression of DeFi innovation, and uncertainty of global competition may all become hidden dangers in the future. However, uncertainty is always the ladder for the advancement of the cryptocurrency market. Risks can be uncertain, but participants are waiting for a certain bull market to come.

Latest news

-

- See more

Bitcoin breaks through 110,000 dollars, regrets and misses of those years

On May 22, the 14th anniversary of Bitcoin Pizza Day, Bitcoin broke through the ...

2025-05-26

2025-05-26

-

- See more

Rethinking Bitcoin's Lightning Network Design from a Thunderbolt Perspective

Why can't I buy coffee with bitcoin?When most people think of Bitcoin, the first...

2025-05-26